Highlights of the annual report 2016 of the CREG

On this page, you can find a summary of a number of important developments and salient facts from the annual report 2016 of the CREG. The full PDF version of the annual report can be downloaded here.

Key developments in national legislation

The most important legal developments in the field of natural gas and electricity in Belgium in 2016 are:

- The further alignment of the gas and electricity legislation with the European third Energy package

- The modification of the support mechanism for offshore electricity

- The revision of the law on the nuclear repartition contribution

The electricity market

An overview of the most important aspects of the electricity market in 2016:

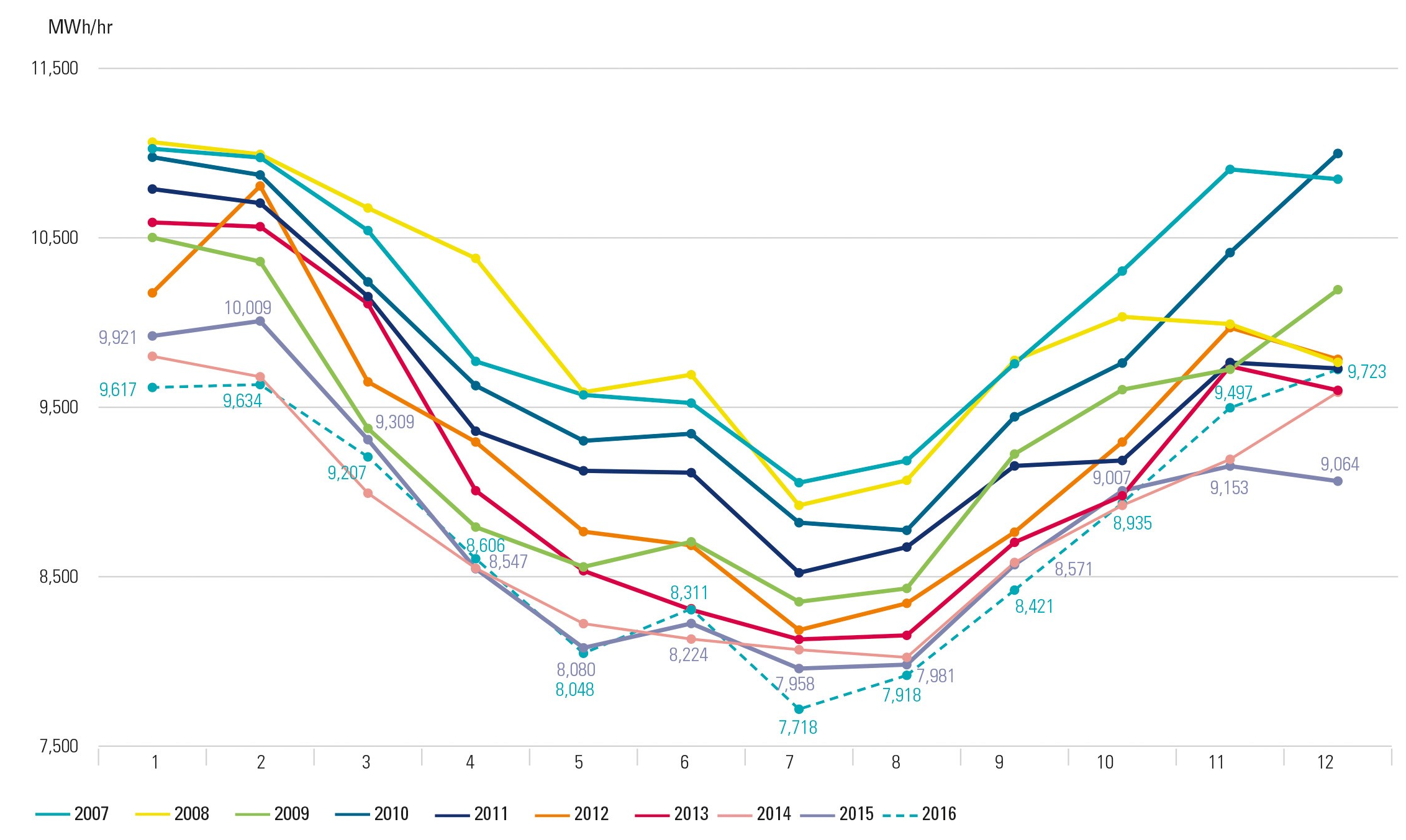

- The economic and financial crisis of 2008 resulted in a significant drop in the electricity load from 2009 onwards. With the exception of the brief upswing in 2010, the downward trend was constant throughout the decade. The lowest annual load was observed in 2016, which was a leap year. From the figure below, which shows this evolution, it appears that the loads of the past three years were the lowest of the decade.

Average load on a monthly basis on the Elia network from 2007 to 2016 (Sources: Elia data, CREG calculations)

Average load on a monthly basis on the Elia network from 2007 to 2016 (Sources: Elia data, CREG calculations) - The offtake from the Elia network amounted to 77.3 TWh and the market share of the wholesale market for the energy generated in Belgium, at 69.5 TWh, reached the highest level of the last three years.

The consequence of this upswing was a sharp decrease (70.6 %) in net imports compared with 2015. This was primarily due to the fact that the nuclear power stations, which had experienced significant problems between 2012 and 2015, generated more electricity. - In 2016, average physical net imports were 732 MWh/h in Belgium. This is a decrease of 70 % compared with 2015 (2 379 MWh/h). This decrease ended the trend of increasing imports which was observed between 2009 and 2015.

- Since May 2015, the calculation and nomination of import and export capacity for the day-ahead market at the Belgian borders has been determined via Flow Based Market Coupling (FBMC). 2016 was the first year in which all imports and exports on the day-ahead market took place via FBMC. Taking into account the relatively high price differences between the CWE countries between October and December 2016, the flows exchanged between the CWE countries remained relatively limited. During this period, France and Belgium together were able to import on average 3 750 MWh/h despite an average price difference with Germany and the Netherlands of €26/MWh. A possible explanation for the limited exchanged volumes can be found in the network, specifically the congestion on the internal transmission lines within the German bidding zone.

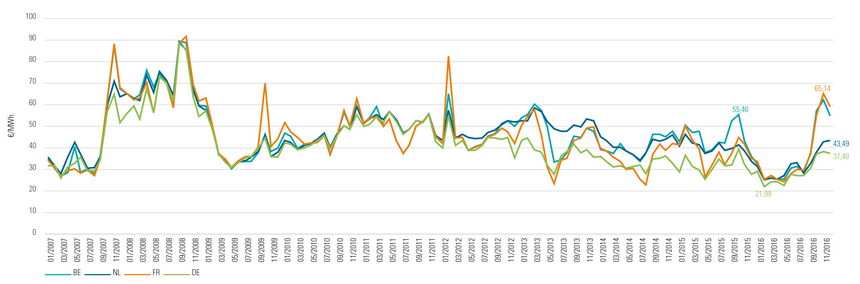

- The average Belgian monthly prices on the power exchanges reached their lowest levels ever in the first eight months of 2016. In fact, the prices were just as low as in the neighbouring countries, i.e. Netherlands and France. The average monthly Belgian market resilience improved over this period. However, in the last four months of 2016, the prices in the CWE region nonetheless rose more sharply in France and Belgium. The resilience deteriorated sharply in October.

Average monthly prices on the power exchanges for Belgium, Netherlands, France and Germany between 2007 and 2016 (Sources: Belpex, EPEX Spot, EEX, CREG calculations)

The CREG continued to stress the consumer protection aspect of its work in 2016.

- It carried out a study of the use of electricity meters on low voltage in Belgium, in which it made recommendations for household consumers and SMEs, to help them choose their electricity meter.

- During the third evaluation of the safety net mechanism, it was ascertained that the development of market shares, the number of changes of suppliers and the market concentration indexes all show that unhindered, growing and genuine competition is now a reality.

- The CREG continued publishing the infographics and monthly dashboard for electricity and natural gas, to provide consumers with all the necessary information to make a reasoned decision.

The REMIT regulation (‘Regulation on wholesale Energy Market Integrity and Transparency’) sets out a series of instructions aimed at preventing and punishing market abuse in the wholesale energy sector. In the context of REMIT, the market participants involved in the second phase of data collection had to register by the start of April 2016 at the latest.

Finally, the CREG defined the objectives which Elia must achieve in 2017 as part of the stimulus referred to in the tariff methodology 2016-2019, to encourage market integration by means of a measured increase in the interconnection capacity made available to the market in the Belgian control area.

The natural gas market

An overview of the most important aspects of the natural gas market in 2016:

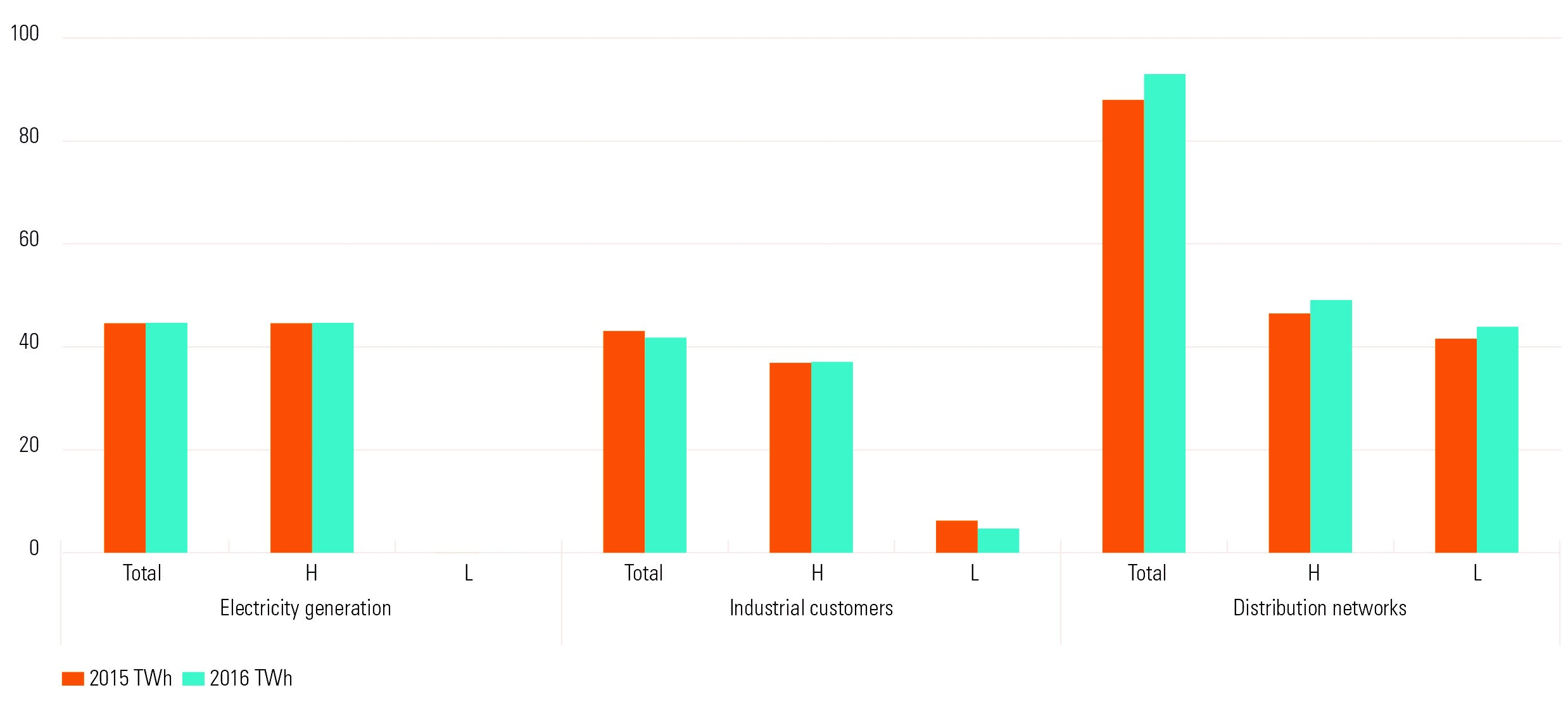

- In 2016, total natural gas consumption rose to 179.4 TWh, which represents an increase of 2.1 % compared with consumption in 2015 (175.8 TWh). The CREG observed clearly higher consumption on the part of end consumers connected to the distribution systems (+ 5.6 %), relatively stable consumption for the power generation (eventually combined with heat production) (+ 0.2 %) and a slight decrease in consumption by industrial customers (- 3.2 %).

Breakdown per consumer segment of Belgian natural gas demand of H-gas and L-gas in 2015 and 2016 (Source: CREG) - At the end of September 2016, the CREG conducted a study about the supply of natural gas to large industrial customers in Belgium in 2015, which represent 28 % of the consumption of Belgian end users. The analysis shows that it mainly concerns short-term contracts (with a duration of 1 or 2 years). In 2015 contract prices were between €18 and €31/MWh. The analysis of average offtake behaviour shows a strong decrease in the annual natural gas offtake from 2009 onwards. The economic crisis that started in September 2008 is the cause thereof. In addition, the aggregate annual natural gas offtake is by nature seasonal. 2010 and 2012 saw the greatest number of changes in suppliers. Between 17 % and 25 % of all industrial customers change suppliers at least once a year. In conclusion, we can state that the market of large industrial customers (including CHP’s) is a dynamic market which is highly competitive.

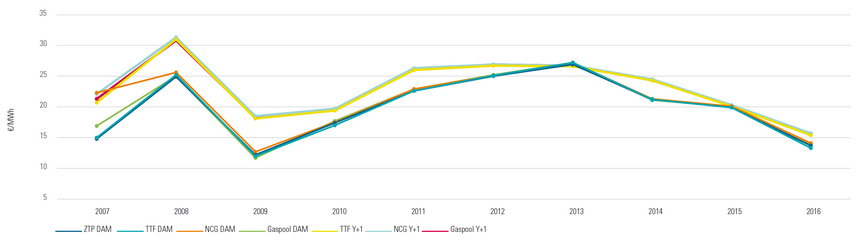

- If we compare the annual day-ahead price (DAM) in Belgium (ZTP), Netherlands (TTF) and Germany (NCG, Gaspool) and the average year-ahead price for natural gas (Y+1) (in €/MW), we can see almost perfect price convergence. This indicates that natural gas can easily be traded between those markets. Given the price convergence and correlation on the short-term market, the long-term price in the Netherlands and Germany can also be used as a reference price for the Belgian-Luxembourg market.

Average annual gas price on the day-ahead and year-ahead market (Sources: CREG, processed data from icis.com, ice.com, eex.com and powernext.com) - The CREG conducted a study on the prices applicable on the Belgian natural gas market in which it analysed market shares, price formation, price levels, price breakdown and billing in the different segments of the Belgian natural gas market in 2015.

- The CREG also established the methodology and criteria for the evaluation of investments in electricity and gas infrastructure and the major risks involved.

- In 2016, the CREG likewise continued to emphasise improving the functioning of the natural gas market, in order to protect the interests of consumers. These aspects are presented in the chapter Electricity.

The CREG

This chapter from the annual report describes, inter alia, the functioning of the CREG and the close relations it maintains with other national and international bodies.

It also contains a list of the acts which the board of directors approved in 2016.